0 or 7 6 6. Argentina Last reviewed 31 August 2022 Registered taxpayer.

Real Property Gains Tax Rpgt In Malaysia And Why It S So Important

The years of assessment to be covered in a tax audit may however be extended depending on the issues identified during.

. Pensions annuities management fees interest dividends rents royalties estate or trust income and payments for film or video acting services when you pay or credit these amounts to individuals including trusts or corporations that are not resident in. Generally any person making certain payments such as royalties interest contract payments remuneration to a public entertainer technical and management fees to non-residents is required to remit the tax deducted at an applicable rate ie. For instance a manufacturing company with a pioneer status tax incentive pays an effective tax at the rate of 72 as only 30 of its profits are subject to tax.

These tax audit frameworks outline the rights and responsibilities of audit officers taxpayers and tax agents in respect of a tax audit. A tax audit may cover a period of one to three years of assessment determined in accordance with the audit focus. Interest on loans granted by third parties or shareholders is liable to investment income tax at 15 and 10 respectively.

A tax withholding agent. Withholding tax to the Inland Revenue Board of Malaysia IRBM within one month from the date of paying or crediting. However from 1 January 2020 foreign service providers of digital services to consumers in Malaysia exceeding MYR500000 per year will be liable to register for Service Tax.

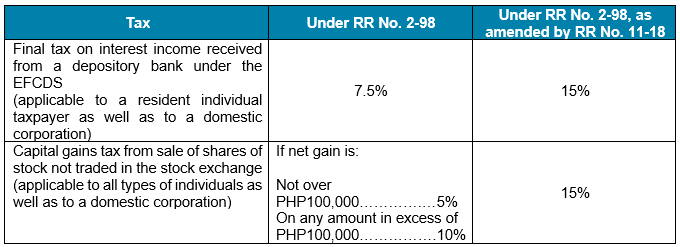

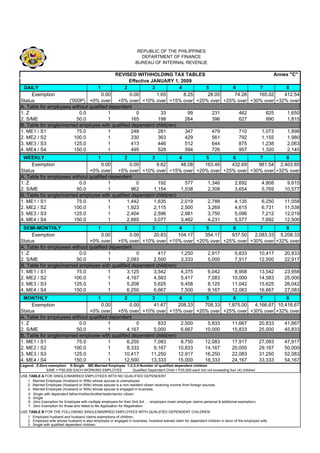

If the gross income is higher than P720000 a 15 withholding tax based on the gross income should be applied. Part XIII tax is a withholding tax imposed on certain amounts you pay or credit to non-residents. Currently an overseas company with no permanent establishment in Malaysia would not be liable to register for Sales Tax or Service Tax.

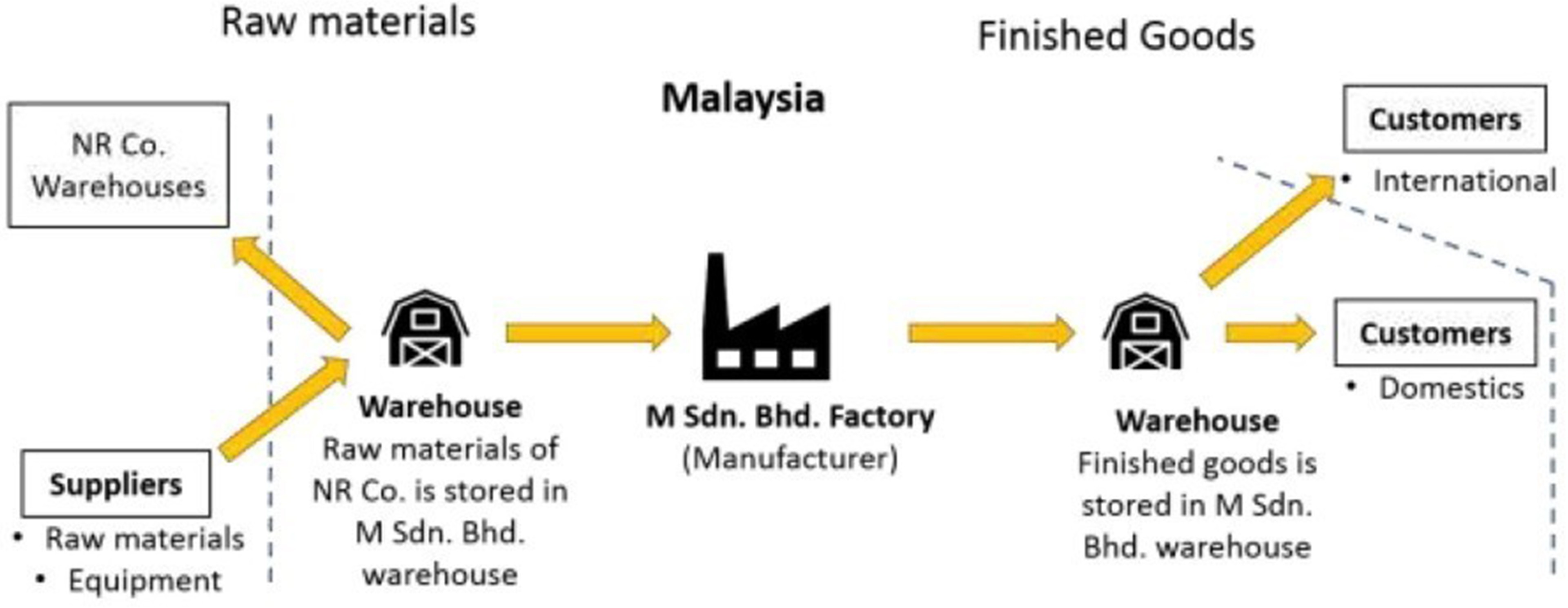

Dividends and royalties are taxed at 10 and the tax is withheld at source by the paying entity in Angola. An individual earning less than P250000 a year is exempted from withholding tax where the income is coming only from a single payor ie. Although Malaysia is neither a tax haven nor a low tax jurisdiction for companies which are eligible for the tax incentives the effective tax rates may be significantly below the normal corporate tax rate of 24.

Tax exemption for individuals earning less than P250000.

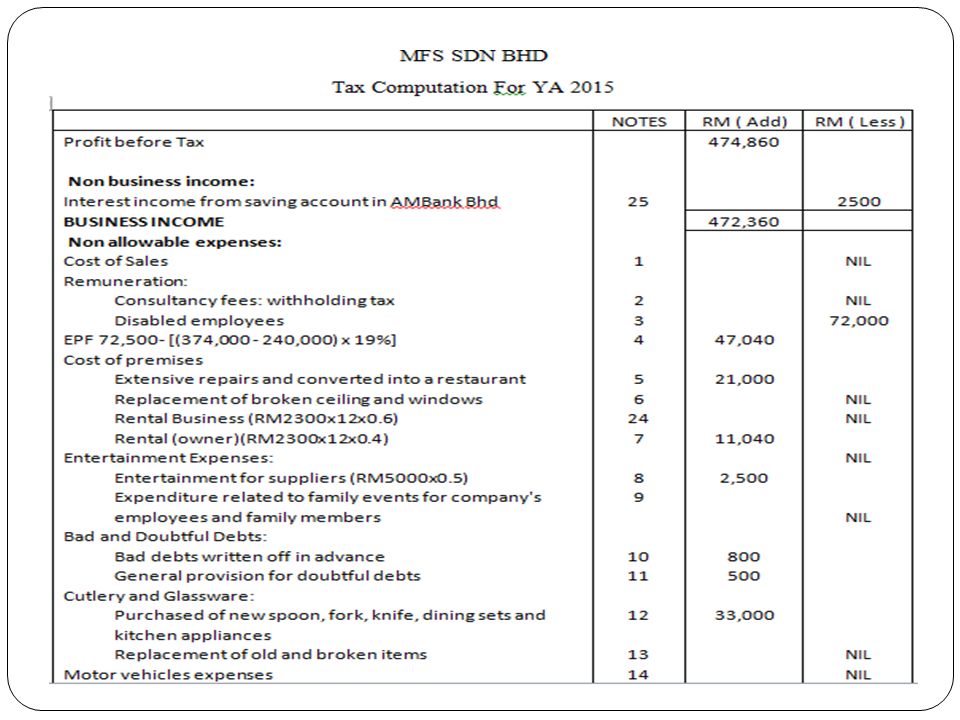

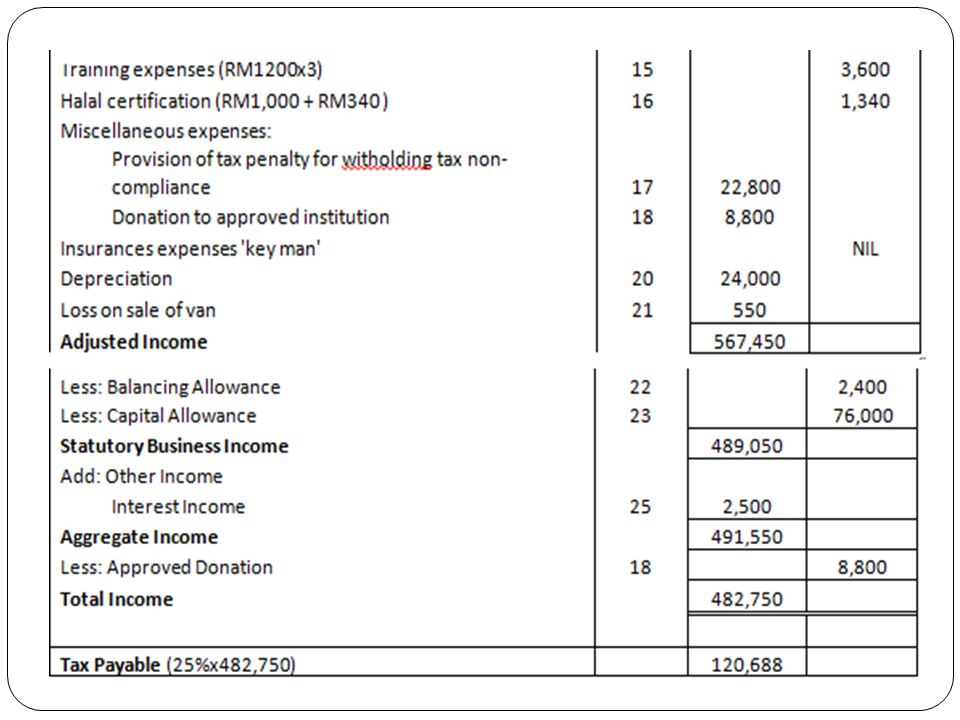

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Tax Clearance For Expats In Malaysia

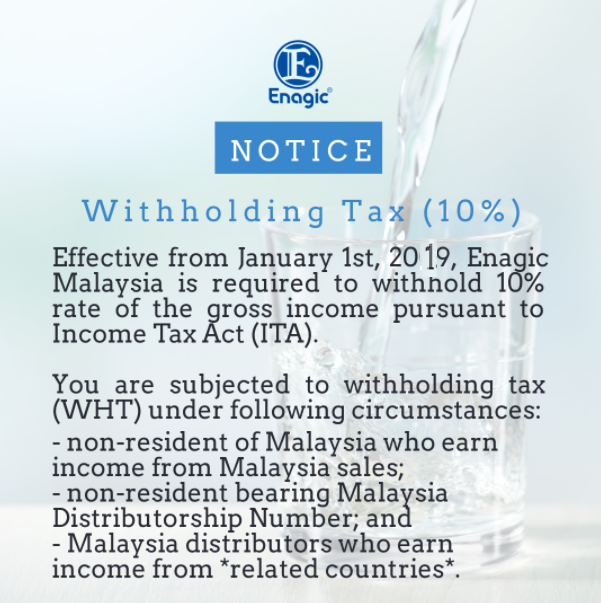

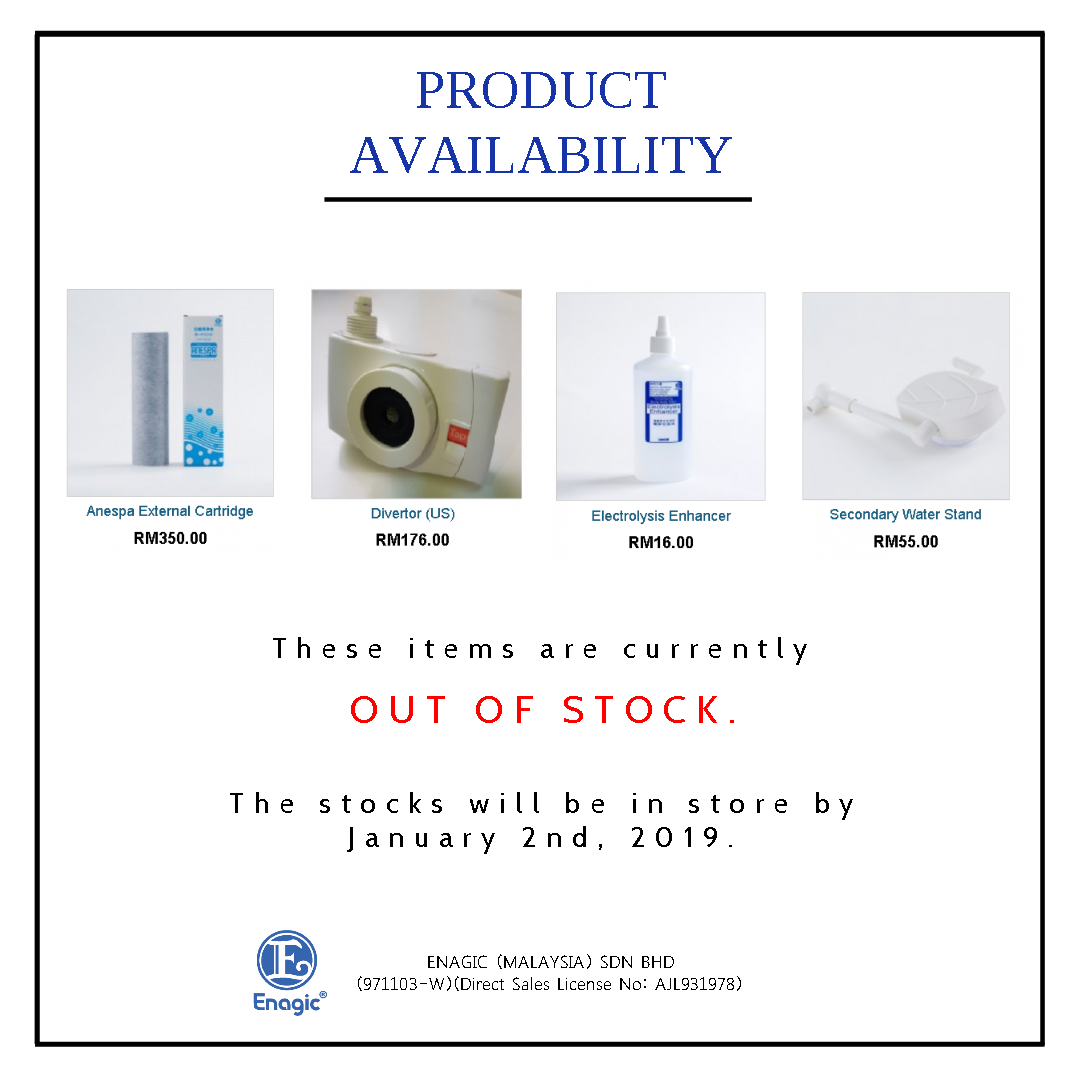

Notice Withholding Tax 10 Enagic Malaysia Sdn Bhd

Train Series Part 4 Amendments To Withholding Tax Regulations Zico Law

Train Series Part 4 Amendments To Withholding Tax Regulations Zico Law

Withholding Tax On Interest Income For Non Resident Company In Malaysia

Train Series Part 4 Amendments To Withholding Tax Regulations Zico Law

Train Series Part 4 Amendments To Withholding Tax Regulations Zico Law

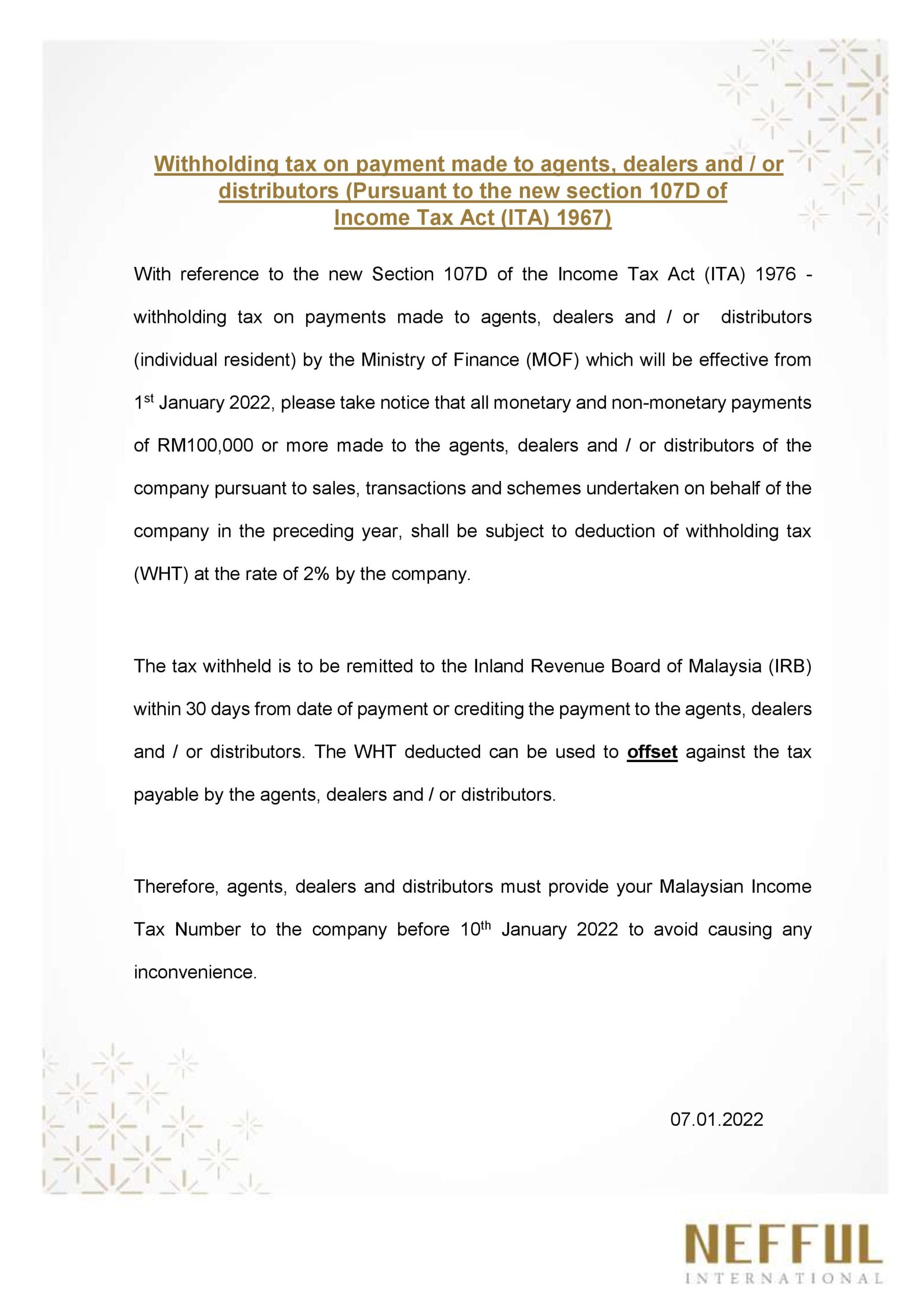

Withholding Tax On Payment Made To Agents Dealers And Or Distributors Pursuant To The New Section 107d Of Income Tax Act Ita 1967 Nefful Malaysia Sdn Bhd

Individual Income Tax In Malaysia For Expatriates

Notice Withholding Tax 10 Enagic Malaysia Sdn Bhd

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

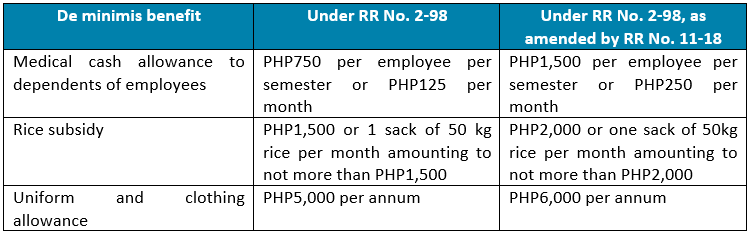

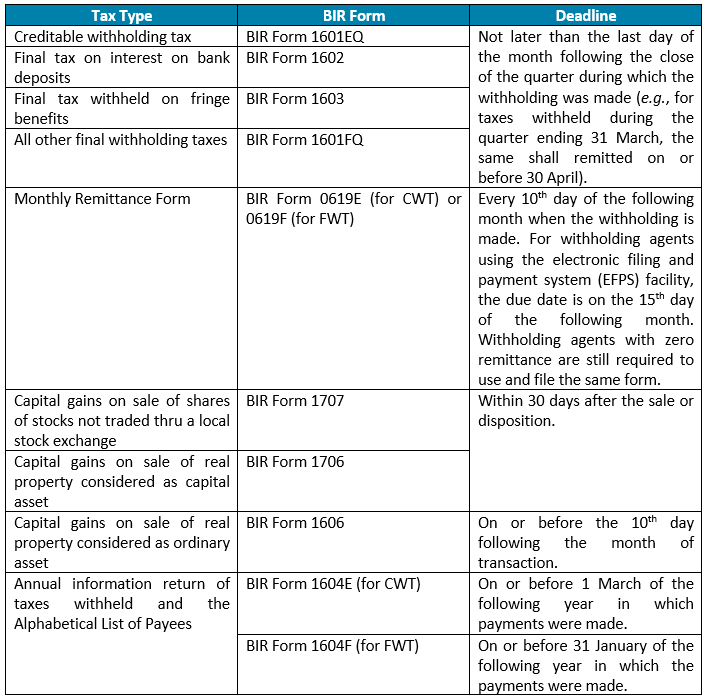

Table Of Withholding Tax Philippines

Train Series Part 4 Amendments To Withholding Tax Regulations Zico Law

Guidelines On Determining If A Place Of Business Exists In Malaysia Ey Malaysia

Atomy Malaysia Withholding Tax Notice Facebook

Finance Malaysia Blogspot Malaysia To Curb Capital Inflows

A Complete Malaysia Withholding Tax Guide